MUDRA Loan for Manufacturing Unit

A Factory Owner with No Collateral Got ₹10 Lakh — Here Is How

Since the launch of the MUDRA scheme, more than 35 crore loans have been disbursed to the micro and small businesses in India, with over ₹23 lakh crore sanctioned. That is an astounding sum – but what is astounding is that not one rupee of this loan was supported by the borrower’s pledge of collateral. Zero. None.

A pickle factory at Morbi. A steel making workshop in Ludhiana. Garment Stitching Unit, Tirupur. It is these types of businesses that have, unnoticed, gradually created income-generating opportunities for individuals, and sometimes small empires, out of funds that even the most ordinary banks would never have granted. The rationale for being funded is one scheme and three tiers:

The credit architecture for micro/ small manufacturing in India today is defined by Pradhan Mantri MUDRA Yojana (PMMY) and its three categories Shishu, Kishor and Tarun.

If you are considering to establish a production unit without belonging to any rich family, this is the first loan product which you should know about MUDRA. It is not because it is easy – it isn’t – but because it is the most accessible credit option for manufacturing entrepreneurs at an early stage. This article explains it in detail.

Source: MUDRA — Pradhan Mantri MUDRA Yojana, Ministry of Finance.

Related Article: How to Get a Government Business Loan in India: Complete Guide to MSME Schemes, PMEGP, MUDRA, and CGTMSE

The Credit Gap That Leaves Manufacturers Stranded

The number of micro, small and medium enterprises (MSMEs) in India is around 63 million. The vast majority (more than 99%) are micro and small businesses. Together these units account for approximately 30% of India’s GDP and a large number of people (more than 11 crore) are employed. Formal credit penetration is, however, very limited, as is to be expected among them.

The credit gap for MSME in India has been estimated to be about $530 billion (about ₹44 lakh crore) by the IFC and World Bank. Which is the gap between what MSMEs require and what they receive from formal lenders. Firms in manufacturing are hardest hit. It is the usual thing that banks require fixed assets, property, equipment, collaterals before they can give working capital and term loans. Those assets aren’t usually at the ready when a first generation entrepreneur is looking to establish a spice processing facility or plastic moulding shop.

This is especially true in states such as Bihar, Jharkhand, Chhattisgarh and Odisha, where manufacturing capability is weaker, and financial literacy remains limited. According to a 2023 SIDBI report, more than 80% of the micro-manufacturing units located in Tier 3 and Tier 4 towns have not received formal credit facilities and had to rely on moneylenders who levy an annual interest rate of 24–36%. That interest cost sucks juice out of margins before a product ships.

It is this gap that MUDRA was created to fill. However, many founders don’t understand the scheme. Many believe it is for traders or service providers only. That is wrong. Production facilities, such as soap factories, steel furniture makers, food processors, and clothing factories are eligible. The scheme’s penetration of manufacturing has been steadily increasing and in the credit flow data reflects this.

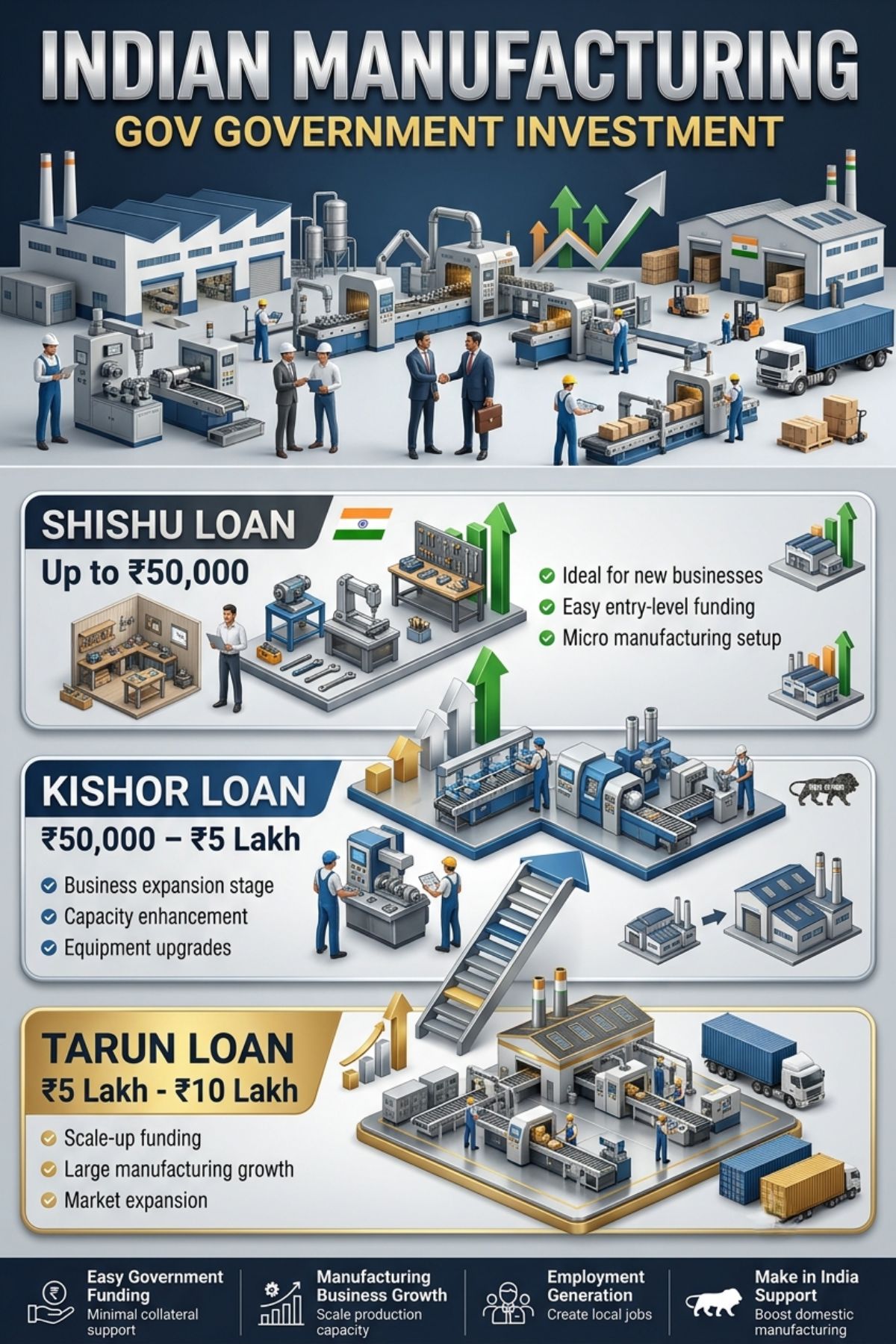

Table 1: MUDRA Loan Tier Comparison — Shishu, Kishor & Tarun

| Category | Loan Range (INR) | Typical Borrower Stage | Interest Rate (Approx.) | Collateral Required | Best Suited For |

| Shishu | Up to ₹50,000 | Seed / Pre-Start Stage | 8–12% p.a. | Nil | Tool purchase, raw material start |

| Kishor | ₹50,001 – ₹5,00,000 | Early Growth Stage | 9–14% p.a. | Nil (below ₹10L) | Machinery, working capital scale-up |

| Tarun | ₹5,00,001 – ₹10,00,000 | Growth & Expansion Stage | 10–14% p.a. | Nil (CGTMSE covered) | Capacity expansion, equipment upgrade |

| Tarun Plus* | ₹10,00,001 – ₹20,00,000 | Established Unit Expansion | 11–15% p.a. | May require CGTMSE cover | Second unit, new product line |

| MUDRA Card | Working Capital – linked to limit | Active Business | Revolving credit rate | Nil | Day-to-day procurement, inventory |

| Women Entrepreneurs | All tiers with priority | Any stage | 0.25% concession | Nil | Female founders get priority processing |

Why Manufacturing Entrepreneurs Should Apply Now

This is a more auspicious time than ever to set up a manufacturing unit at the micro level, due to three policy changes.

Firstly, the government has been nudging all the public sector banks, regional rural banks (RRBs), microfinance institutions and small finance banks to go ahead with disbursement of the MUDRA loans concurrently. This does not imply that you’re standing in one line. There are more than 40 types of lenders nationwide to turn to. Banks such as SBI, Bank of Baroda, Punjab National Bank and Canara Bank are allocated MUDRA counters and have dedicated relationship officers at the clusters of manufacturing areas in the districts.

Second, the PM Vishwakarma Yojana, which was started for artisans and traditional craftsmen, has paved the way for collateral-free loans of up to ₹3 lakh at a concessional interest rate of 5% — and it is linked to the MUDRA ecosystem. Some manufacturing businesses employ traditional methods of production, such as blacksmithing, carpentry, pottery, or tailoring garments, that require skills, and may therefore be eligible for both programs.

Third, the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) provide guarantee cover for MUDRA loans — especially at the Kishor and Tarun levels. This is what makes it possible even without any collateral. The premium is modest (0.37–1.35% annually for the size of the loan), and are usually included in the cost of the loan.

The Udyam Registration Portal (udyamregistration.gov.in) has introduced a facility for instant registration of Udyams and this is one of the important documents in the MUDRA application. Registration takes less than 20 minutes, and unlocks access to the entire gamut of MSME schemes, other than MUDRA.

Turn your budget into a successful business plan

Step-by-Step: How to Apply for a MUDRA Loan for Your Manufacturing Unit

Step 1: Register Your Business

First, register for Udyam. Free, Online and based on Aadhaar and PAN. This will enable you to avail the MSME status and will be required for most of the applications of MUDRA that are above ₹1 lakh. Do so first before heading to any bank.

Step 2: Choose Your Tier and Amount

Do not overestimate the amount of funds that you require. If you are buying your first machine or if you are buying raw material for the start, then Shishu is the best option for you as it is up to ₹50000. Kishor (₹50,000 to ₹5 lakh) pays for machinery, deposit for the shed, and three months working capital. Tarun (₹5 lakh – ₹10 lakh) is for partially operational units which require expansion funds – a second machine, a packaging line or inventory buildup.

Step 3: Prepare Your Documents

- Aadhaar Card and PAN Card (self and business)

- Udyam Registration Certificate

- Business registration documents (business registration certificate or deed of partnership)

- Last 6 months Bank statements (even a savings account will do for Shishu)

- 2 passport photographs

- Quotes from machinery/equipment supplier (for Kishor/Tarun)

- Business plan or project summary (1-2 pages; there are templates available at NPCS and entrepreneurindia.co)

- Note: If applying as SC/ST/OBC (priority processing) a cast certificate is required.

Step 4: Approach the Right Lender

Please do not enter unauthorized branches. Please contact beforehand and request to speak with the loan officer from the MUDRA section. Many of the branches have corresponding MSME desks in the major manufacturing clusters like Rajkot, Coimbatore, Surat, Kanpur, Meerut, Howrah. For loans at the Shishu level, MFIs (microfinance institutions) are frequently more effective in disbursing loans than banks. PSU banks offer better rates to Kishor and Tarun.

Step 5: Submit Application via MUDRA Portal or Directly

The Udyami Mitra portal provided by RBI (udyamimitra.in) is linked to various banks and a person can apply to several banks at once or walk into the bank directly. Processing time: Shishu loans can be sanctioned within 7-15 working days. Duration of the loans is 20-45 working days for Kishor and Tarun loans, depending on the level of documentation.

Step 6: Post-Disbursement — Use Funds as Declared

Purpose-specific loans are called MUDRA loans. Once declared funds for machinery purchase, purchase the machinery. Invoices or utilisation certificates may be required from banks. The misuse of the funds from MUDRA loans is considered as a violation of loan covenant and it may impact on your credit record. Keep business current account separate.

Typical time frame of Udyam Registration to first production (Kishor loan): 60-90 days if documents are clean.

Get Detailed Insights from This Book: Select & Start Your Own Industry

Table 2: Investment Breakdown for a Sample MUDRA-Funded Manufacturing Unit

(Example: Small Food Processing Unit — Spice Grinding and Packaging)

| Investment Head | Shishu (₹) | Kishor (₹) | Tarun (₹) | Source / Notes |

| Primary Machinery | 20,000–40,000 | 1,50,000–3,00,000 | 4,00,000–6,00,000 | Domestic suppliers, states like Punjab/Maharashtra |

| Raw Material Stock (3 months) | 5,000–10,000 | 50,000–1,00,000 | 1,50,000–2,50,000 | Local mandi / wholesale suppliers |

| Shed / Space (deposit + 3 months) | Nil (home-based) | 30,000–60,000 | 60,000–1,20,000 | Industrial estates offer subsidised rent |

| Packaging & Labelling Equipment | Nil | 20,000–40,000 | 50,000–1,00,000 | Available from SME equipment dealers |

| Working Capital Buffer | 5,000–10,000 | 30,000–60,000 | 90,000–1,30,000 | Retain in account for 60-day cycle |

| Misc. (licences, transport, contingency) | 2,000–5,000 | 20,000–40,000 | 50,000–80,000 | FSSAI ₹2,000 basic; Udyam = free |

| TOTAL ESTIMATE | ₹32,000–65,000 | ₹3,00,000–5,40,000 | ₹8,00,000–12,80,000 | Adjust for state and product type |

Financial Snapshot: What the Numbers Look Like

The figures are for a small food processing unit setup with the financial support of Kishor in a 400-600 sq ft unit in a Tier 2 city.

Capital expenditure: ₹3.5-5.5 lakh (Machine + raw material + setup). Monthly operating costs: ₹40,000-65,000 (raw material, manpower for 2-3 people, electricity costs, packaging, logistics).

Revenue at 60% capacity: ₹75,000–90,000/month. Revenue at 100% capacity: ₹1.20–1.60 lakh/month.

The gross margins of food processing are usually between 28% and 38%. Net margins after deducting all overheads and loan repayment: 12-18% at 60% utilisation and 18-24% at full capacity with loan partially repaid.

Payback period: 24-36 months (for a Kishor scale unit on the basis of consistent 70%+ capacity utilisation). In a majority of cases, the tenure of MUDRA is 3-5 years with the start of EMI six months after the loan is disbursed — confirm with your lender.

Don’t make assumptions from month 1 that they will be 100% capacity. Most units achieve a realistic ramp, defined as 40% by Month 1, 60% by Month 4 and 80% by Month 8. Make cash flow plans around that curve.

Table 3: Government Schemes That Support MUDRA-Funded Manufacturing Units

| Scheme | Administered By | Benefit Relevant to MUDRA Borrowers | Link / Portal |

| PMMY (MUDRA Yojana) | Ministry of Finance / MUDRA Ltd. | Primary loan up to ₹20 lakh — no collateral | mudra.org.in |

| CGTMSE | SIDBI + Govt. of India | Credit guarantee cover for loans up to ₹5 crore | cgtmse.in |

| PM Vishwakarma Yojana | Ministry of MSME | Concessional credit at 5% for artisan manufacturers | pmvishwakarma.gov.in |

| PMEGP | KVIC / State Govt. | Subsidy of 15–35% on project cost for new units | kviconline.gov.in/pmegp |

| Udyam Registration | Ministry of MSME | Mandatory MSME identity for all scheme access | udyamregistration.gov.in |

| Stand-Up India | SIDBI / Banks | ₹10 lakh–₹1 crore for SC/ST/Women manufacturers | standupmitra.in |

| SFURTI | Ministry of MSME | Cluster-level support for artisan and rural manufacturers | sfurti.msme.gov.in |

Planning Your Unit? NPCS Can Help You Build the Foundation Right

A well-drafted project report is all the more crucial for entrepreneurs who are coming out of the Shishu stage, especially for those who are aiming for Tarun loans, or are intending to avail MUDRA along with PMEGP subsidy for their business. Accessed at niir.org and entrepreneurindia.co, Niir Project Consultancy Services has been serving the manufacturing entrepreneurs for more than 45 years by providing detailed project reports (DPRs), techno-economic feasibility studies, plant layout designs, machinery sourcing and other relevant information and end-to-end consultancy for the first time start up entrepreneurs. For anyone looking to establish a food processing unit, chemical plant, agro-processing unit or any other MSME manufacturing unit and requires a bankable project report, that can be presented to the lending institutes and committees of the Ministry of Food Processing Industries NPCS is a credible source to explore to fulfil the requirement.

Get Detailed Project Report (DPR): Project Reports & Profiles

Entrepreneur Spotlight

Renu Devi, Varanasi, Uttar Pradesh Renu runs a handloom and cotton garment stitching unit employing 7 women in a semi-urban cluster near Varanasi. She started with a ₹45,000 Shishu loan from a regional rural bank, upgraded to a ₹2.5 lakh Kishor loan 18 months later, and now generates a monthly turnover of ₹1.1 lakh. Her key lesson: “Apply early, even if you are not fully ready. The process teaches you what your business actually needs.” She is now exploring a Tarun loan to add a digital embroidery machine.

Your Next Step Is One Application Form Away

For the ones with a manufacturing idea and a spot – whether or not it’s a leasing area or a shared shed – you’ve got sufficient to start the MUDRA process. There is no need to place any collateral on the loan. It doesn’t require the business to have a lengthy history. It requires a good plan, clean paper and a banker who believes you know what you’re doing.

Visit the Udyami Mitra portal today. Enter your Udyam Registration no., (If you have not obtained it, visit udyamregistration.gov.in). Choose Kishor/Tarun as per your need. Apply for a mortgage with three lenders at the same time. Your bank is the one that will respond the quickest.

Don’t wait for ideal circumstances. The funded manufacturer also began with a simple basic plan and small shed last year. The scheme is live. Funds are available.

Frequently Asked Questions (FAQ)

1. What is the maximum loan amount under MUDRA for a manufacturing unit?

The standard MUDRA maximum under the Tarun category (PMMY framework) is ₹10 lakh. A newly launched MUDRA extension called Tarun Plus can offer up to ₹20 lakh to expand an eligible existing unit. Beyond this limit, if you’re a manufacturer and looking for amounts over ₹20 lakh without collateral, consider term loans from PSU banks, backed by the Credit Guarantee Fund for Micro and Small Enterprises (CGTMSE), which can go up to ₹5 crore.

2. What licences does a manufacturing unit need before applying for a MUDRA loan?

The bare minimum you need is an Udyam Registration (it’s free at udyamregistration.gov.in). If you’re into food processing, you’ll also need a basic FSSAI Registration (₹100/year). If your unit risks causing pollution, you’ll need Consent to Establish (CTE) from the State Pollution Control Board. If your unit has 10 or more workers and uses power, it comes under the Factories Act and needs a Factory Licence. And while it’s not an absolute prerequisite for a MUDRA loan, once your turnover is expected to cross ₹20 lakh annually, you’ll need to get GST registration.

3. Where can I source raw materials for a small manufacturing unit in India?

That depends totally on your product! For spices and agro inputs, try the wholesale mandis in Unjha (Gujarat), Khari Baoli (Delhi), and Vashi (Mumbai). For steel and metals, seek out secondary dealers in places like Mandi Gobindgarh (Punjab) or Bhiwadi (Rajasthan). When you have to pack, ensure you look out suppliers from Silvassa, Hapur (UP) & Daman. Don’t neglect to see for suppliers under the govt e- Marketplace (GeM) – here in too are a variety of suppliers affiliated with government departments (many provide general goods).

4. Is a MUDRA loan profitable enough to justify the setup cost for a manufacturing unit?

Absolute yes for the loan categories – Kishor and Tarun in the majority of manufacturing industries! As a majority of manufactured products like food processing, apparel, packaging materials, light engineered goods earn between 12% and 24% as net margin the loan is feasible. A five year, five lakh Kishor loan might have a EMI between Rs 5,500 and Rs 12,000 per month, that should easily manageable if your unit makes about Rs75,000- Rs1.5 lakh a month in your business from the third month, assuming capacity utilization stays at 65-70%.

5. Can SC/ST and women entrepreneurs get any special benefit under MUDRA?

Absolutely! Women entrepreneurs receive a 0.25% interest rate subsidy on all MUDRA loan categories. SC/ST applicants get favoured processing at many PSU banks and are also eligible for subsidies under the Pradhan Mantri Employment Generation Programme (PMEGP), typically ranging from 25% to 35% of project costs for rural SC/ST beneficiaries. In fact, the Stand-Up India Scheme also enables SC/ST and women entrepreneurs to get term loans ranging from ₹10 lakh to ₹1 crore from scheduled commercial banks to set up new greenfield manufacturing units.

6. How can NPCS help me apply for a MUDRA loan for my manufacturing unit?

NPCS is the company which can let you develop one detailed bankable Detailed Project Report (DPR). Usually when you’re seeking for MUDRA lenders or when presenting your plan to committees that government set, a good Detailed DPR is generally preferred. It comprises various reports detailing your projected finances, specifications about machinery and materials required, market study, etc. For more details visit niir.org or entrepreneurindia.co for a report relevant to your business.

{kind=link}