PMEGP loan rejection reasons

The Opportunity Is Real. So Is the Rejection Rate.

Each year thousands of first-time entrepreneurs come to the banks with great ideas and an application for PMEGP. Under the scheme, interest will be given at a discounted rate of up to ₹25 lakh for service projects and ₹50 lakh for manufacturing businesses. In theory it is the ideal way for a new business to launch in government-funded environment. But in reality, banks have a 88% rejection rate on their applications. It’s no myth that number. This is a fact that consultants and MSME advisors experience annually in various states such as Uttar Pradesh, Rajasthan, Maharashtra, and Tamil Nadu.

So, what goes wrong? It is fair to say this: The problem is seldom the entrepreneur. It’s the paperwork, the project report and how the banker sees it will be financially viable. This article outlines the actual reasons behind rejections — and what serious applicants need to do differently.

Related Article: PMEGP Loan 2026: How to Apply, Eligibility & Subsidy Amount

What PMEGP Actually Offers — And Why Banks Are Still the Gatekeepers

The Prime Minister’s Employment Generation Programme (PMEGP), under the Ministry of MSME is handled by Khadi and Village Industries Commission (KVIC). The scheme offers interest free margin money subsidy of 15% to 35% of the project cost as per the category and area of the Applicant. The rest of the project will be funded from a bank loan.

It is here that structural tension starts. The banks are commercial lenders. They consider applications for government compliance, credit risk, ability to repay, and collateral. PMEGP will not supersede these banking conventions. In addition to a traditional loan, it provides a subsidy. If you don’t have a project that looks like a bankable project, it will be rejected, even if it meets all the eligibility requirements.

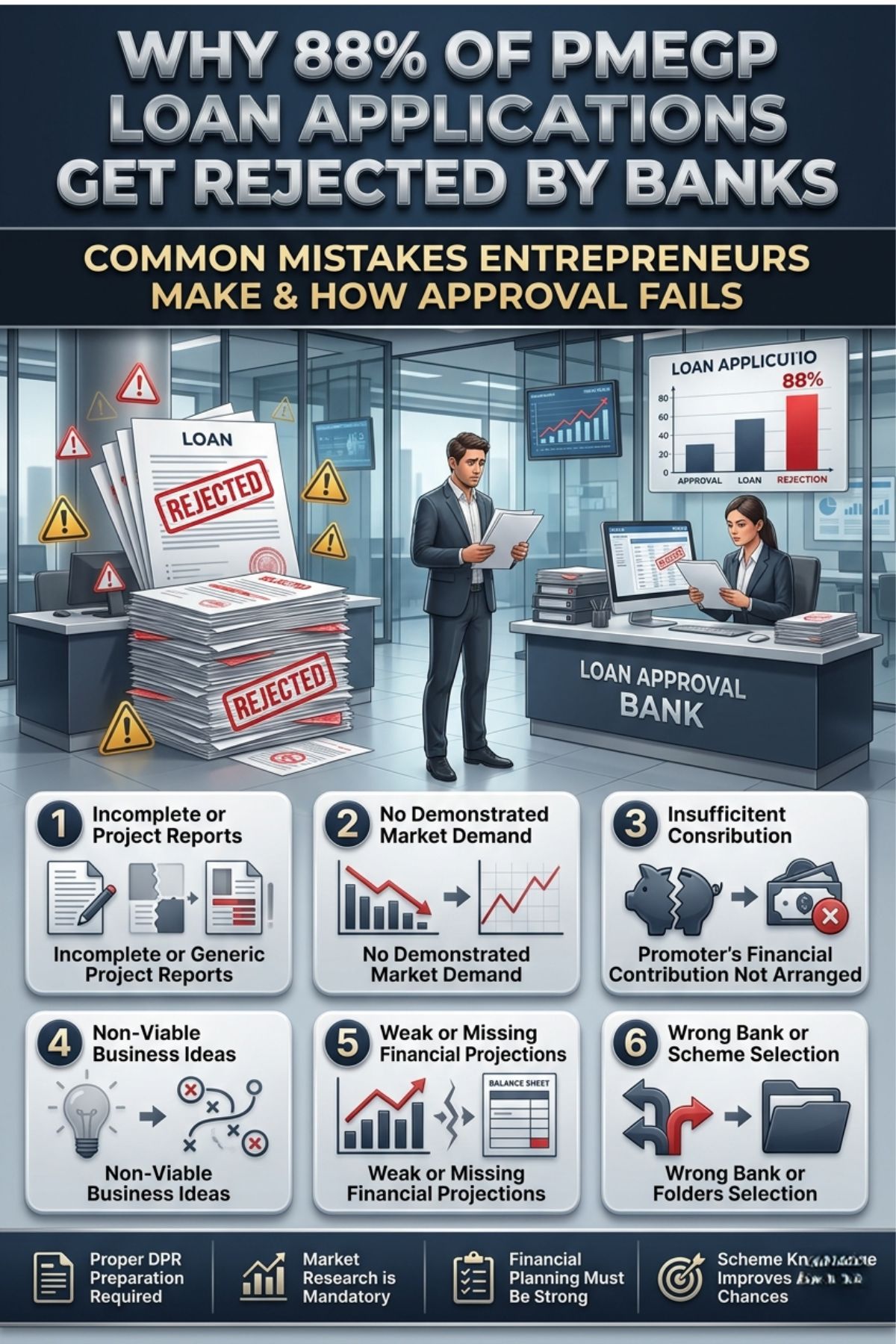

The 6 Real Reasons Behind That 88% Rejection Rate

1. Incomplete or Generic Project Reports

This is the No. 1 reason for the failure of PMEGP applications. Most of the applicants present a simple project summary, which is a few pages of some costs and a paragraph on the market. These reports are sent to the bankers and they see hundreds. They quickly recognize when a report doesn’t go deep enough. To do this, the banker must have detailed financial projections without which it is not possible to evaluate risk, a credible demand analysis, clear capacity utilisation assumptions and machinery specifications. Hence, they just say no.

A Detailed Project Report (DPR) is NOT an option – it is a requirement! This is the main document which transforms the loan seeker into a bank’s credit worthy entrepreneur. The Ministry of MSME has multiple times stressed the importance of quality documentation in achieving the success of disbursal under PMEGP.

2. No Demonstrated Market Demand

The number one question bankers ask is whether this business will make enough money to pay back the loan? In absence of a convincing market demand analysis, preferably with trade data, consumer trends, and local demand estimates, the banker cannot justify the loan. Most of the applicants go through this section without thinking about it, or just copy and paste some boilerplate from the web. It doesn’t work every time.

One of the most important considerations made by the Office of the Development Commissioner for MSME (DC-MSME) while appraising the applications received under PMEGP is the market feasibility.

Read the Complete Book Here: Just For Starters: How To Become A Successful Businessman?

3. Promoter’s Financial Contribution Not Arranged

The applicant is required to provide margin money, which would generally be between 5% to 10% of the project cost, depending on the type of PMEGP. A lot of applicants think that they can handle it later. Banks don’t share the assumption. The promoter’s contribution is not clearly pledged then the bank regards the application as incomplete. This is the rejection of even technically strong projects.

4. Business Ideas Chosen Without Viability Logic

Many applicants choose a business ideas category from what a neighbour or relative recommended – they don’t take into account whether there’s a market, raw materials supply or a competitive situation. This is something that banks notice right away. If the banker asks the applicant why he/she has gone into this particular type of business and the answer he/she can give cannot be answered with assurance and data, the meeting is effectively over. DPIIT’s startup framework revealed that selection of projects are highly influential in achieving better funding because the projects are in line with the local market realities.

5. Weak or Missing Financial Projections

The financial model in a PMEGP DPR should consist of 5-year forward-looking profit and loss statements, balance sheets, cash flow statements and break-even analysis. A lot of applicants will only include one page of a cost estimate and this is what they’ll be called financial planning. The promoter must demonstrate to the bankers the flow of funds into and out of the business. If not, the entrepreneur just hasn’t taken the time to seriously consider the business.

MSME lending guidelines from the Reserve Bank of India also clearly refer to project financial viability as a necessary criterion for priority sector MSME loans.

6. Applying to the Wrong Bank Branch or Scheme Category

These loans are channelized through scheduled commercial banks, regional rural banks (RRB) and cooperative banks. The experience of all the branches is not of the same order when it comes to PMEGP processing. Many candidates come to a general branch without knowing if the branch in which they go is active in the disbursement of PMEGP loans. Also, the selection of the wrong project category (manufacturing/supplier or urban/rural) can influence the calculation of subsidies and eligibility criteria. An automatic scrutiny is triggered when there is a mismatch between the type of project and the category of the scheme.

What Approved Applicants Do Differently

There are some similarities among the 12% who are accepted. They usually come along with a well-done DPR which includes all technical, financial and market aspects that the banker requires. They show that they’ve done their homework on their business. They bring their own contributions ready, their own capital settled, and a well-defined repayment programme incorporated into the financial scheme.

Also, successful applicants will typically contact MSME Development Institutes (MSMEDIs) or registered consultants to be able to validate their project reports prior to submission. The National Institute for Micro, Small and Medium Enterprises (ni-msme) operates training and DPR assistance programmes tailored for the benefit of the applicants of PMEGP.

Import–Export Opportunity Aligned with PMEGP Projects

Export opportunity is one of the areas of under-leveraging in the project planning of PMEGP. There are many manufacturing industries that are exportable and are eligible under PMEGP including food processing, agro-processing, handicrafts, light engineering and herbal products etc. Entrepreneurs with export-ready projects make better projections to provide to banks.

According to data collated by the Federation of Indian Export Organisations (FIEO), India’s contribution to MSME exports is more than 45% of the total merchandise exports. Export business projects have a better chance of survival as the banks will show interest in the project as it has diversified risk of revenue due to the international demand and hence the dependence on domestic market is less. The inclusion of export projections, even though they make up a small proportion of planned revenue in Year 1 (10-15%) makes a meaningful contribution to the loan appraisal score.

Get Detailed Project Report (DPR): Ayurvedic Herbs & Natural Products Guide

Indian MSME Success Stories — What the Numbers Actually Prove

Mansukhbhai Prajapati — Mitticool

Mansukhbhai Prajapati, the founder of Mitticool, started his business from a micro unit as a refrigerator manufacturer and built his business around the building of refrigerators with clay. He began with an idea of a handcrafted product and a small investment and developed a traditional craft into an export enterprise and a business with potential for growth. His main takeaway message for PMEGP applicants: The business idea is not as important as the logic of making the business viable. It seemed impossible — until he created the documentation for his DPR that made it possible to fund and scale a clay refrigerator.

Jayaben Desai — Self-Reliant SHG Model, Gujarat

In Gujarat, the journey of Self-Help Group to MSME for Jayaben Desai is a testament to the fact that even in the service sector, applicants can scale up their businesses in a short period of time. Her team started with a small PMEGP-backed unit for the production of packaged foods. Tightness in the operational cost model and meticulous demand validation were key to the success. Her unit is now a source for contemporary retail establishments. The key takeaway: Planning for market linkages within the DPR directly affects bank confidence.

Deep Industries Ltd — Started as a Small Unit

Now a listed company, Deep Industries Ltd started as a small engineering and energy services company. Paras Savla, the Founder, has always spent time on the project feasibility analysis at each and every expansion phase. That discipline of treating every new project as a full-fledged and a technical-financial evaluation, is just what turns a PMEGP application into a bankable project.

Stop guessing—choose the right business with confidence

How NPCS Helps Entrepreneurs Break Through the 88% Barrier

Decades ago, at Niir Project Consultancy Services (NPCS), we have worked with many entrepreneurs whose business ideas were good, but for various reasons their project documents were missing and they were not able to get PMEGP loans approved.

We provide Banks with professional Market Survey cum Detailed Technical Economic Feasibility Reports (DPRs) as per Banks Appraisal requirement. Our reports contain detailed manufacturing processes, verified market demand analysis, process flow diagrams, product mix and capacity planning, complete specification of all machinery and raw materials and complete five-year profit projections along with breakeven analysis and profitability analysis.

Our goal is straightforward: show entrepreneurs that they are economically feasible, profitable, and can be sustainable in the long run prior to entering a bank. A properly prepared NPCS DPR not only makes it easier to get approvals, it alters the banker’s perception of the promoter. You don’t request money from an applicant, but walk in as a business case entrepreneur. That separation makes a difference!

PMEGP Project Data — Key Reference Numbers

| Parameter | Manufacturing Projects | Service / Trading Projects |

| Maximum Project Cost | ₹50 Lakh | ₹25 Lakh |

| Subsidy (General Category, Urban) | 15% of Project Cost | 15% of Project Cost |

| Subsidy (SC/ST/OBC/Women/NER, Urban) | 25% of Project Cost | 25% of Project Cost |

| Subsidy (General Category, Rural) | 25% of Project Cost | 25% of Project Cost |

| Subsidy (SC/ST/OBC/Women/NER, Rural) | 35% of Project Cost | 35% of Project Cost |

| Promoter Contribution (General) | 10% of Project Cost | 10% of Project Cost |

| Promoter Contribution (Special Category) | 5% of Project Cost | 5% of Project Cost |

| Bank Loan Component | Remaining after subsidy + contribution | Remaining after subsidy + contribution |

| Estimated Application Rejection Rate | ~88% (documented) | ~88% (documented) |

| Primary Rejection Cause | Inadequate DPR / No Demand Study | Inadequate DPR / No Demand Study |

Frequently Asked Questions (FAQs)

Q1. What’s the most frequent reason for my PMEGP application being rejected?

The most likely reason is that the project report is not up to mark. Bankers require a comprehensive DPR including a market demand analysis, financial projections and technical specifications. They do not consider a basic summary to be an appraisal. The vast majority of rejections occur at the DPR (dossier preparation) evaluation phase — and before the banker looks at the promoter’s profile!

Q2. Is it possible to reapply if rejected by PMEGP?

Yes, it is possible to re-apply. But the same documentation will usually only result in the same outcome when re-applied. To get the project accepted again, the specific reasons for rejection must be taken care of, which is usually done by improvements in the project report, arranging the promoter’s contribution, and fixing mismatches in categories.

Q3. Should I hire a consultant to create my PMEGP DPR?

Although it is not required, the proper preparation of a DPR will benefit the chances of getting approval. Bank appraisal standards consultants know just what bankers expect in the way of financial projections, demand analysis and technical details. A well-prepared DPR is a key component of the success for many approved applicants.

Q4. Which bank has good bank for PMEGP loans?

Public Sector Banks like Bank of Baroda, Punjab National Bank and State Bank of India have higher PMEGP disbursements volume. PMEGP loans are also processed by Regional Rural Banks (RRBs) especially for rural borrowers. The main thing to keep in mind is selecting a branch which actively processes PMEGP applications – so inquire from the branch manager about the PMEGP disbursement experience before applying.

Q5. What is the time taken for the approval of the PMEGP?

It takes approximately 30 to 90 days from the time of full application to process. Typical delays occur when there is incomplete documentation, pending EDP training certificates or slow queues to the internal bank appraisal process. Making sure your application is complete in all ways shortens this process.

Q6. Will there be a repayment of PMEGP subsidy?

The PMEGP subsidy on margin money is not to be repaid, as long as the unit is in operation for the lock-in period agreed with KVIC, which is normally three years. In case of the closure of the unit or the business stops functioning during the lock-in period, the amount of subsidy can be recovered by the bank.

Conclusion: The 12% Who Get Approved Know Something the Others Do Not

PMEGP is not a scheme of the government, but a real one and well-funded for the first-generation entrepreneurs. It has been designed to facilitate just the type of businesses that India has a need for – local manufacturing, agro processing, handicrafts and service businesses. However, the funding pipeline runs through banks. Banks do not make loans based on enthusiasm, either.

The high rejection rate of 88% is not meant to condemn the scheme. It’s a clue to the way that applicants document. The DPR is a real business tool and not a form to fill in, and entrepreneurs who use it consistently as such, always break through. The answer is not to work more on the application. It’s with regards to the project report, it’s a matter of working smarter.

{kind=link}