Auto Components Manufacturing Business in Maharashtra

More passenger as well as commercial vehicles are manufactured in Maharashtra than any other state in India with Pune, Nashik, Aurangabad and Chakan-Talegaon facilities operated by Tata Motors, Bajaj, Mahindra and numerous OEMs operating from around the world. It is not the concentration of the vehicles that is a problem, it is the demand for components that Maharashtra’s own supplier base has not been able to meet until now. A business in the Auto Components Sector built by the Maharashtra entrepreneurs today is located in the biggest captive buyer ecosystem in the country which gives them a strategic advantage of placing the JIT delivery in front of the plant of the OEMs instead of a logistics problem.

It’s not a sector that is ripe for discovery — Pune’s supplier ecosystem is decades old — but the tier-two and tier-three component layer is a place where global OEMs increasingly want to bring in the second or third qualified domestic supplier — and that’s where a founder with the right technical focus and quality discipline can insert himself/herself.

Get Detailed Project Report (DPR): Automobile Industry & Auto Components Guide

Why Maharashtra’s Auto Corridor Is a Genuine Opening

The main point is the concentration by the OEM. Pune has only Tata Motors, Bajaj Auto, Mahindra & Mahindra and a host of international suppliers such as Bosch, along with Cummins, and the place of Aurangabad and Nashik has additional assembly and component manufacturing. That density made it economically viable for the component manufacturer to not chase the buyers around the country, as the buyers are in a hundred-kilometre radius, mainly in the estates built by the Maharashtra Industrial Development Corporation, the state’s industrial infrastructure arm.

This is further strengthened by government policy. The EV Policy and the overall industrial promotion scheme in Maharashtra provides capital subsidy and stamp duty exemption to EV component manufacturers, especially those providing components used in EVs, a space where global OEMs are aggressively looking for new domestic suppliers over the slower to react internal combustion component makers. Central schemes are superposed over this and go through the Ministry of Micro, Small and Medium Enterprises.

The entry capex depends on the complexity of the component. The manufacturing cost of a basic sheet metal or forging component unit is about 10-15 crores while that of precision machining and/or EV-specific electronic component units is 25-40 crores due to tighter tolerances and testing requirements. Estates of MPCB/MIDC licensing will normally enable licensing within 8 to 12 months, which is considerably quicker than when licensed on its own, especially in the already established industrial parks. The stocks of production and exports from the sector as announced by the Confederation of Indian Industry are a good cross check before sizing a new line.

Business Selection Logic

The margin structure is greatly influenced by the substitutability of a component. Fasteners and basic stampings that are generic, made by dozens of companies that already supply from the Pune belt, come in at eight to fourteen percent gross margin. Twenty to thirty percent of the time, it is precision parts that require special tooling and OEM qualification, but without that qualification, switching to a new supplier has a real cost to requalify the precision part that OEMs do not incur unless the quality is truly failing down.

The typical path to scalability in this industry is not one of the founders’ own production ramps, but rather through the OEM qualification cycles. Usually, the new supplier begins with one component for one OEM, and will prove their quality across several thousand units before he/she will move to additional components or a second OEM.

Risk focuses in the OEM order cyclicality, or how the volume of vehicles produced ebbs and flows with the business cycle of the OEM, which the component manufacturer is not able to control, and in the investment in tooling, which cannot easily be transferred to different OEMs if a vehicle order is cancelled.

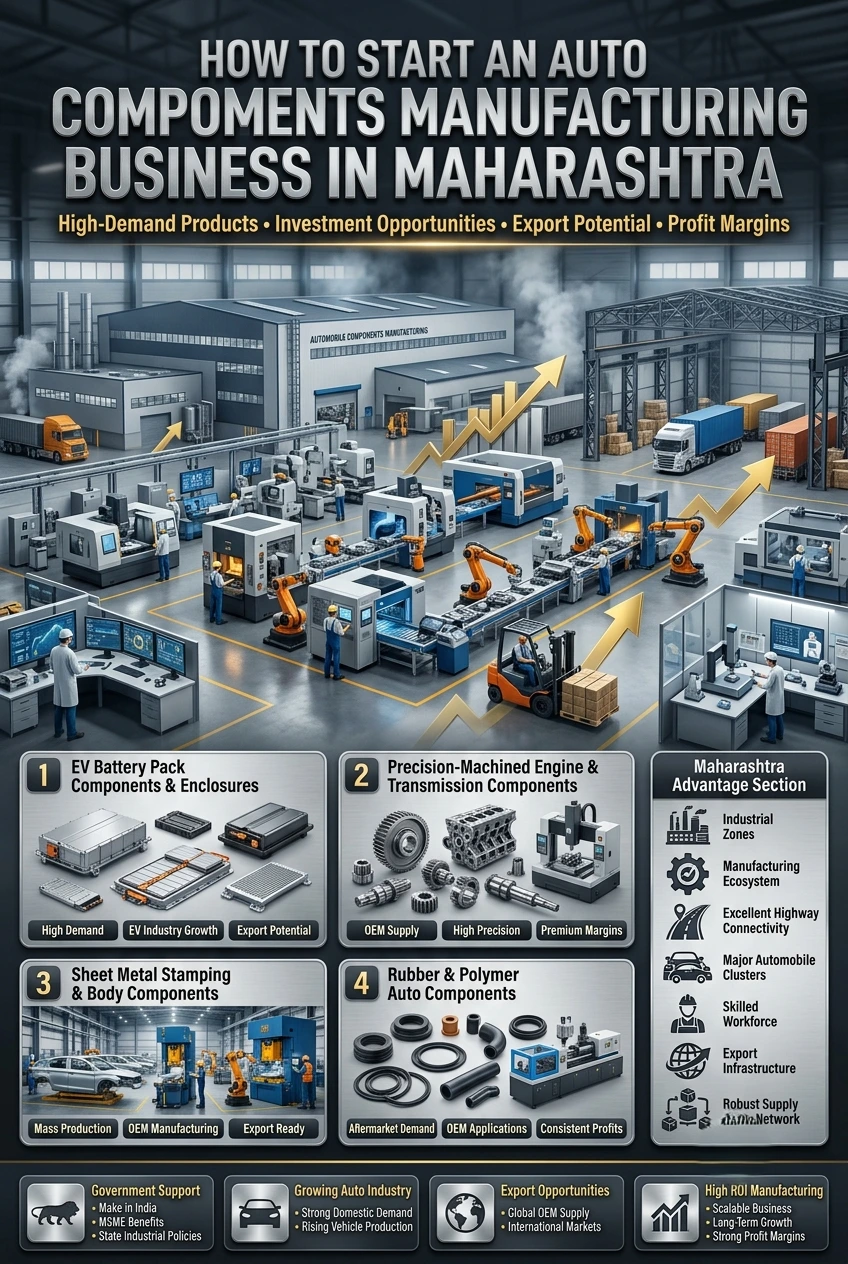

Product and Project Opportunities Worth Evaluating

EV Battery Pack Components and Enclosures

In response to the state’s push towards the production of EVs, the state has also offered subsidies to EV component manufacturers, which has led to real demand for battery pack enclosures, thermal management components, and connector systems that current suppliers of internal combustion engines have been slow to completely retool. It takes between eighteen and twenty-five lakhs of crore rupees in capex investment to build a dedicated line for EV OEMs and battery pack assembler. With a twenty-five to thirty-two percent margin, it is technically new and there is no real scarcity of qualified domestic suppliers in this category.

Explore This Book: Handbook on Production, Recycling of Lithium-Ion and Lead-Acid Batteries

Precision-Machined Engine and Transmission Components

As EV transition picks up speed, there continues to be a consistent demand for precision manufacturing, which is still ongoing for automotive components, including engines and transmissions, at commercial vehicle manufacturing units in Maharashtra and those for export. A CNC-based precision machining unit, with a capex of the tune of Rs 15 to 20 crores directly caters to Tier-1 suppliers and OEMs. The margins are eighteen to twenty-four percent and there are opportunities for export to the European and South East Asian auto markets, once ISO/TS quality certification is achieved.

Sheet Metal Stamping and Body Components

Body panels and structural parts stamping is the most highly-commoditized and most volume-intensive segment of Maharashtra’s auto parts industry. If the unit is for mid-volume OEM supply requirements, it requires capex in the range of 10 to 15 crore rupees and is targeted at plants within logistics-friendly distance. With intense competition margins are 8-14%, so this is not a margin play, unless a founder can find a truly captive anchor buyer, where they can rely on the volume and confidence that the customer will return.

Rubber and Polymer Auto Components

Rubber gaskets, seals and polymer-based parts for the interior continue to retain steady demand in all vehicle segments that the state produces and the category is expected to provide a return to specialization in certain formulations of compounds for which fewer suppliers can be found consistently. It requires the capex of 8 to 12 crore for a dedicated unit, both for OEMs and aftermarket replacement parts market. Margins are sixteen to twenty-two percent and the aftermarket channel provides a cushion of demand when the OEM is off production.

Related Article: EV Auto Component Manufacturing in India: A Profitable Startup Opportunity

Indian Entrepreneurs Who Built This

The key is that Baba Kalyani invested in Bharat Forge early on precision manufacturing and quality export production instead of just focusing on local volume demand, and today the company is one of the world’s largest forging manufacturers. It is that export discipline that was established long before the majority of Indian component producers thought to seriously consider overseas customers.

Arvind Poddar gave Balkrishna Industries its own unique specialisation – off-highway and specialty tyres – and turned it into a worldwide specialty tyre exporter from an Aurangabad manufacturing unit instead of fighting with the big boys in the commodity passenger tyre business. Abhay Firodia’s Force Motors (Pune) also succeeded in carving out a niche in specialized commercial and utility vehicle manufacturing along with supplying components to car manufacturers, indicating that a mid-size manufacturer from Maharashtra could compete profitably if they had identified a niche market and entered the business. Narrow specialization, with export quality discipline, always beats broad component differentiation in all three in this auto corridor that’s already full.

Import-Export Opportunity Analysis

The auto component industry already makes a significant contribution to export to Europe, North America and Southeast Asia, especially for forging and precision-machined components and specialty tyres to these destinations. However, India as a whole continues to import a substantial number of components specifically used in EVs, such as battery management electronics and some sensor systems, as the qualification of their domestic suppliers for such newer categories is still limited.

A founder with an EV component qualification strategy can benefit not only from the benefit of being able to offer an essential component for the EV industry in his home market, but also from exporting potential as global OEMs look to diversify the sources of their components from China. The export licensing and product classification is handled by the Directorate General of Foreign Trade, and the fact that both Nashik and Chakan are close to the ports of Mumbai and Pune means that logistics costs remain low when this is a company that plans to focus on export markets from its inception.

Turn your budget into a successful business plan

Government Reference and Feasibility Planning

The fuel and utility economics of any manufacturing unit within this corridor are linked to the overall petroleum and refining economics in India. In the Annual Report 2024-25 of Ministry of Petroleum and Natural Gas, Government of India (mopng.gov.in), it’s worth noting that the domestic refining capacities are feeding industrial fuel and lubricant supply chains, which are being utilised by component makers that appear to be quite distant from the petroleum business, at a scale that can be seen from the report.

The serious founders who are interested in the business generally order a Market Survey cum Detailed Techno-Economic Report before the order of machinery. These are prepared by Niir Project Consultancy Services, and they are specifically for industrial manufacturing entrants, and include process flow, machinery and raw material specification, capacity planning and complete project financials – replacing a number that an OEM procurement team or bank can evaluate with an assumption. Invest India and the Federation of Indian Chambers of Commerce and Industry both have automotive manufacturing briefings that are good to read in both the context of automotive industry and also when claiming incentives on a state level.

Conclusion

Entrepreneurs of auto component manufacturing companies don’t need to fight with Bharat Forge or Bajaj’s existing supplier network head-to-head. It must know which component category to engage, preferably one other than EV, since there is a definite policy direction in the state, and develop a track record of qualification for the OEM that will enable a one-shot contract to become a multi-year relationship.

The decision hierarchy is simple. Situated in or near an existing MIDC industrial estate to reduce logistics cost and time for approval. When technical ability permits, select a precision or specialty part rather than a commodity part and the margin difference is usually more than 10 percentage points. Allow 6 to 12 months’ runway for OEM qualification cycles, and regard this as a cost of entry, not a delay.

The auto corridor in Maharashtra continues to be the biggest captive component demand pool in India and the EV transition has been actively creating new slots for suppliers which the legacy internal combustion component makers have been tardy in filling. This is one of the most trustworthy manufacturing points in India for a founder who truly has an OEM qualification rigging precision manufacturing capability and the endurance to clear the qualification properly.

Capex vs Margin Overview by Component Category

| Component Category | Capex Range | Gross Margin | Target Buyer |

| EV Battery Pack Enclosures | ₹18-25 Cr | 25-32% | EV OEMs & battery assemblers |

| Precision Engine/Transmission Parts | ₹15-20 Cr | 18-24% | Tier-1 suppliers & OEMs |

| Sheet Metal Stamping/Body Parts | ₹10-15 Cr | 8-14% | Assembly plants (volume buyers) |

| Rubber/Polymer Auto Components | ₹8-12 Cr | 16-22% | OEMs + aftermarket |

Frequently Asked Questions

Founder-centric – action-oriented, decision-making questions:

Which are the actual capex and qualification of auto components manufacturing business in Maharashtra OEMs?

The price of a basic sheet metal/forging line ranges from about ten to fifteen crore rupees while the precision or EV specific component lines require twenty-five crore rupees minimum due to the stricter tolerances and test rig requirements.

What is the process for a new supplier to become an OEM?

It usually takes 6 to 12 months for the samples to be approved, the quality audits to be completed, and the production trials to be run. Don’t count on income the day you commission, this is a fixed expense of entry.

Are the risks of EV components manufacturing higher than those of regular auto components?

It carries risk to technology but has a much lower degree of competition, as not many domestic suppliers are qualified at present. Conventional components are competing with the established competition but with more predictable and proven demand, it comes down to a founder’s appetite for risk and their capital runway.

What is the greatest threat in this industry?

OEM order cyclicality. Production volumes ebb and flow with the wider demand cycle over which the component maker has no control; and tooling spent on any particular OEM is not readily available to be transferred between customers if a contract expires, so it’s important to diversify OEM relationships early on.

Which of the following categories has the greatest room for a first-time player?

Precision parts and components for the electric vehicle market provide the biggest margins from eighteen to thirty-two percent, due to the less-than-abundant qualified domestic competition. Commodity stampings provide more consistent volume and significantly reduced margins.

{kind=link}