Compressed Biogas (CBG) Plant

India’s energy transition story now has a chapter called biomass that is worth of betting. CSB plants use agricultural residues, cattle dung, municipal solid waste, and food processing wastes, to produce pipeline quality gas. This is NOT experimental technology. It’s commercial reality. Data from the Annual Report, 2024-25 of the Ministry of Petroleum and Natural Gas (MPNG), Government of India, indicates that 100 CBG and Biogas plants, having a total production capacity of approximately 700 metric tonnes per day, have already been commissioned. CBG is being supplied to industrial customers in 54 geographical areas of the City Gas Distribution network and is being sold from 315 retail outlets.

The timing Favors first movers. Thousands more units are needed to achieve national targets. The Ministry of Petroleum and Natural Gas has designed SATAT to allow entrepreneurs to enter this segment with guarantees for offtakes, priority sector loan periods, with phased blending to be ramped up from 1% in FY 25-26 to 5% from 28-29. Entry barriers are there; capex is from ₹15 crore to ₹30 crore, depending on feedstock and scale; but policy tailwinds and margin potential make it one of India’s better manufacturing wagers in its alternate fuel economy.

Get Detailed Insights from This Book: Biogas and Compressed Biogas (CBG) Production Handbook (from Waste & Renewable Resources)

Why CBG Manufacturing Makes Business Sense Now

Basic building blocks add up. India generates 62 million tonnes of municipal solid waste (MSW) every year. Add another 500 million tonnes of crop waste and 3 billion tonnes of cattle dung. Add another 500 million tonnes of crop waste and 3 billion tonnes of cattle dung. It is not used for many purposes and most of it is burned in open fields or left to rot at landfills. CBG plants make revenue of this waste stream. The amount of biogas produced from one tonne of feedstock is about 50-60 cubic meters and after purification, it can generate 25-30 kg of CBG. As a byproduct of the plant, fermented organic manure can also be sold for ₹1500 per tonne market development assistance from the Department of Fertilizers.

Expressions of interest have been floated by oil marketing companies to find CBG suppliers for 20-year offtakes. The procurement prices are between ₹46-54 per kg, which are based on crude benchmarks. This cancels out risk on the demand side with serious players. CBG projects are classified by the Central Pollution Control Board under ‘White category’ upon case-to-case basis and the projects enjoy minimal regulatory hassles if they adhere to the environmental standard.

RBI’s priority sector classification opens the avenues of financing. CBGs are now considered as agriculture allied activity and term loans are available at concessional rates from banks. Entrepreneurs without their own capital can sell out their business at 70:30 debt/equity ratio. Central Financial Assistance from MNRE National Bio-Energy Program me is available for all types of CBG and biogas plants for a part of capital expenditure.

Import substitution logic reinforces the argument. 55% of crude oil requirement is met through imports in India. Each tonne of CBG substitutes for imported natural gas or CNG. Decentralized Biogas production is in sync with the Government’s target of achieving ‘Net Zero’ by 2070 and the ‘Swachh Bharat Mission’. The urban local bodies actively search for partners for their plants based on municipal solid waste. When logistics and feedstock aggregation problems can be addressed then municipal corporations will often lease land and make waste supply agreements available.

Understanding Project Economics and Capex Structure

The requirement for land for a standard 10 tonne per day CBG plant is 2 – 3 acres. Civil construction, anaerobic digesters, gas purification units, compression systems and biomass handling equipment make up 60-70% of the total project cost. Feedstock supply chains will require moderate working capital needs once they begin to stabilize. Take 3 months of operating expenses as buffer.

Recurring costs are largely feedstock cost. Agricultural residue can be collected at a price of ₹1500-2500/tonne in the region and season. Cattle poop may be more economical, and sometimes free, if you’re able to arrange deals with dairy farms that want to get rid of their poop. Municipal solid waste supply agreements can even consist of tipping charges you pay to the municipality for waste disposal. The compression, chilling and auxiliaries cost ₹3-5 per kg of CBG production. The cost structure is completed by manpower, maintenance and interest service.

The break-even period is usually 4-6 years depending on the feedstock, capacity utilization, and debt terms. Well-executed projects fall within a range of IRRs of 16% – 22%. The actual value comes from additional byproduct value streams: selling fermented organic manure to farmers, trading carbon credits in Clean Development Mechanism schemes, and negotiating industrial supply contracts at higher prices.

To scale, it’s important to learn 2 disciplines: feedstock aggregation, plant uptime. The most efficient systems are operating at 85-90% utilization. There must be a reliable feedstock supply on a daily basis. If feedstocks haven’t been diversified, crop residue availability may be variable and limit production during certain seasons. Smart operators combine three to four waste types—paddy straw, municipal waste, dairy slurry, and food processing rejects—in order to reduce the volatility of waste supply.

Get Detailed Project Report (DPR): Biotechnology, Biofertilizers, Enzymes and Biogas

Concrete Project Opportunities Under CBG Manufacturing

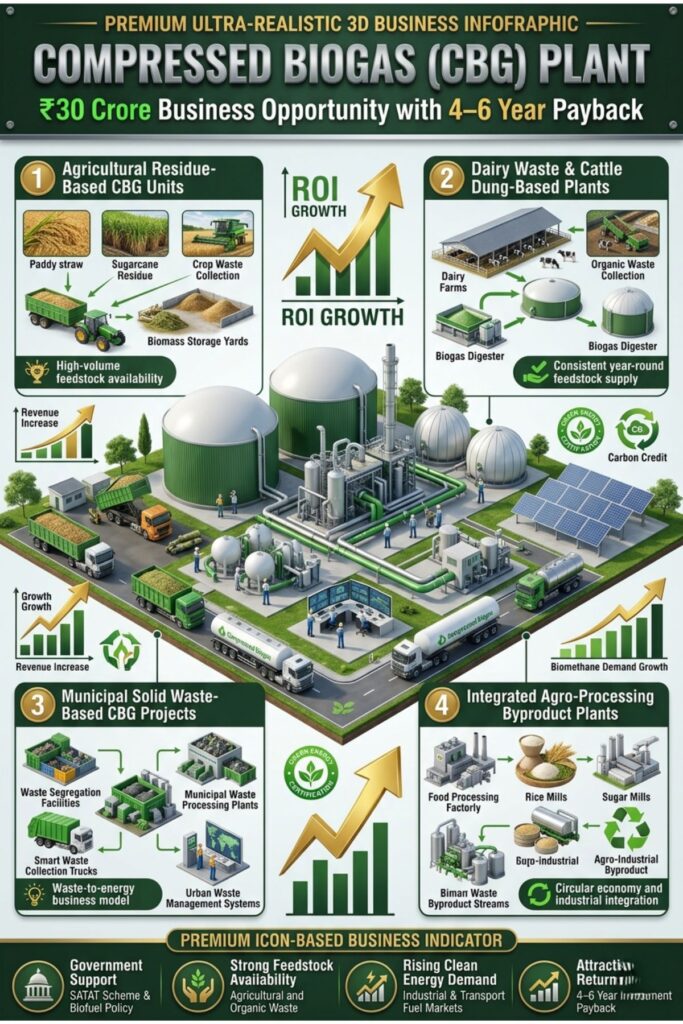

Agricultural Residue-Based CBG Units

Increase planting in rice and wheat belt areas such as Punjab, Haryana, western Uttar Pradesh. The capex for a plant of 5 tonne per day capacity for processing paddy straw and wheat stubble is about ₹15-18 crore per day. Offtake is guaranteed by oil marketing companies. The most difficult aspect is collecting the isolated farm waste. Cooperate with farmer producer organizations or commission aggregation machinery as part of the government’s biomass collection scheme. Gross margins are around 25-28% with the stabilization of feedstock procurement. CNG stations, industrial users and CGD operators are the categories of buyers. This model is best suited for rural-industrial complexes where the labor force is not too expensive and the distance to be covered for reaching retail centers is less than 100 km.

Dairy Waste and Cattle Dung-Based Plants

The number of cattle is 303 million in India. Thousands of tonnes of slurry are produced by the large dairy cooperatives in Gujarat, Rajasthan, Maharashtra and Uttar Pradesh every day. A plant for processing 10 tonnes a day, which is to be attached to a 5,000-animal dairy farm, requires an investment of ₹22-25 crore. If the dairy is an equity partner, then feedstuff cost is not a significant cost. This configuration yields high quality CBG with stable methane percentage. Organic manure in fermentation state is easy to sell to organic farming networks. Feedstock procurement cost also significantly decreases, bringing the margins to 30-32%. Scale up by creating multiple copies of the model on cooperative dairies. Amul’s biogas projects prove how cooperative model reduces risks in implementation.

Municipal Solid Waste-Based CBG Projects

The organic waste produced per day in Metros and Tier-2 cities is 60-70 tonnes per lakh population. The CAPEX for a municipal waste plant is ₹35-40 crore per day for a plant of 20 tonnes per day. Urban local bodies offer land, waste supply contracts and in some cases guarantees for the tipping fees. The Swachh Bharat Mission, Urban 2.0 provides extra Central support. Municipal waste processing is a solution to two issues: Waste disposal for the city and energy generation for you. This is due to increased costs for pre-processing items, such as the segregation, shredding and removal of contamination, which puts pressure on margins at 18-22%. However, municipal contracts provide revenue visibility over the long haul. Identify cities with landfill emergencies and strong political support for waste-to-energy investments. Select cities that have landfill problems and political interest in waste-to-energy investments.

Integrated Agro-Processing Byproduct Plants

Organic waste from food processing units such as rice mills, sugar factories, fruit pulp making factories has a high biogas yield potential. The cost of a 7 tonne per day plant, when located with a rice mill processing 10,000 tonnes of rice per year, is ₹18-20 crore. Feedstock: Captive rice husk, broken grains and parboiling effluent. CBG can operate the mill’s boilers, or can sell to other customers. The margins of this integrated model are 24-26%, and no feedstock transportation is required. Focus on areas of high concentration of rice processors in AP, TN and WB. This is good news for agro-processors as the waste disposal liability is converted into a revenue stream whilst reducing their fossil fuel bills.

Related Article: Compressed Biogas (CBG) Plants: A Bankable Green Energy Business for New Entrepreneurs

Learning from Indian Entrepreneurs Who Made CBG Work

Praj Industries, a brainchild of Pramod Chaudhari, is an Indian company that was the first to introduce second generation biogas technology in India. The company set up multiple CBG projects using agro-industrial waste and municipal solid waste. Their decision-making process focused on technology localisation, that is, developing digesters to meet the requirement of Indian feedstock diversity instead of introducing European technology. The takeaway: match the technology to the local context, don’t impose foreign solutions. Chaudhari’s execution playbook laid focus on feedstock contracts before commissioning of plants, something many startups fail to do.

Adani Total Gas ventured into the CBG business by integrating biogas into the CGD network in Gujarat. They did not vertically integrate all the steps but instead formed partnerships with local waste aggregators, their “scaling model. This asset-light strategy helped to speed up the deployment. For smaller entrepreneurs, the lesson: don’t have to own the entire value chain. Work with feedstock providers on revenue-sharing basis. Focus capital on the conversion plant, not on building a feedstock empire.

German-Indian joint venture (GIJV) company Verbio India has one of the biggest straw-based CBG plant in India, located in Bhubaneswar. The key to the insight of the Founder Claus Sauter was to mechanize the handling of feedstocks to 100%. The majority of Indian plants have to be shut down due to manual handling, which causes bottle necks in the harvest period when feedstock supply is high. Production continuity was ensured with Verbio’s investment in automatic baling, transport and feeding systems. CapEx for mechanization is a return on investment due to uptime improvements. Do not under invest in material handling infrastructure.

How Indian CBG Startups Can Tap Export and Substitution Opportunities

The demand of natural gas in India is more than 160 million cubic meters per day of natural gas of standard measurement at 15°C and 1bar.India’s natural gas consumption is more than 160 million cubic meter of natural gas at 15°C and 1bar of standard measurement. Domestic production is just 50% or less. This imbalance is filled by high cost imports of LNG. One tonne of CBG replaces one tonne of imported gas. With CGD networks growing in to 400+ districts, the demand for pipeline injectable Biogas will grow. Production to match pipeline specifications, at least 90% methane, controlled moisture and hydrogen sulfide, will bring in high prices from gas utilities.

Adoption of Bio-CNG vehicles is gaining momentum. To reduce diesel expenses, commercial fleet owners, particularly in the public transport and last-mile delivery sectors, are making the switch to CNG. CBG blends can be used in CNG without engine modification at a blend concentration of 1-5%. The distribution companies will scramble for sourcing CBG which is compliant with the requirements of blending, effective from FY 2025-26. Locate your plant within 150 km of high traffic CNG corridors in Delhi-NCR, Mumbai, Pune, Ahmedabad or Bengaluru.

There is export potential in the carbon credits generated from biomass. International buyers are willing to pay $8-12/tCO₂ avoided. The 10MTD CBG plant is able to reduce the release of methane gas from decomposing waste and substitute fossil fuels, thereby saving about 12,000 – 15,000 tonnes of CO2 for every year of operation. Sign up your project for the Clean Development Mechanism or Verified Carbon Standard. The additional revenue from carbon credit can enhance project bankability by 3-5%.

One other is for exports of organic fertilizer to the markets of Southeast Asian and African countries. Enriched CBG plants’ organic manure that is fermented is selling at premium prices in the export market, particularly with nitrogen-phosphorus-potassium. Establish collaborations among agri-export houses for packaging of FOM with the organic vegetables and fruits. This spreads out the income over time and protects against the fluctuations in prices for CBG.

Navigating Regulatory and Execution Risks

Even with policy support, risks are associated with execution. The biggest failure point is the feedstock procurement. When farmers are willing to sell the crop residue, then they sell it to anyone who pays cash right away. With spot prices rising during harvest, long-term supply contracts break down. Start building buffer inventory for 45-60 days. Or even get contracts from different aggregators, which will make you not rely on a single source.

The decision of what technology to use is more important than entrepreneurs realize. The chemistry of anaerobic digestion depends on the feed. Cattle dung needs mesophilic digestion (35-37°C), crop residue thermophilic digestion (50-55°C) and municipal waste robust pre-treatment of plastics and metals. Do not purchase “typical” plant design. Use engineering companies who have been in your feedstock area. IOCL, BPCL and HPCL have a vendor list of approved technology providers.

Connectivity with the grid, and offtake logistics, can be overlooked. For bottled CBG, tanker transport will be necessary if the plant lies more than 25 km away from the nearest CGD pipeline/cNG station. This translates to a reduction of margins by ₹4-6 per kg in delivered cost. Coordinate cost sharing of transporting to buyers, or locate plant within a piping distance of infrastructure. The government has announced CBG-CGD synchronization scheme for financial assistance for pipeline connectivity; apply early.

Environmental clearances are required. The effluent treatment, leachate management and odor control are under the close watch of State pollution control boards. The cost range of effluent treatment systems that are in compliance is ₹50 lakh to ₹1 crore. Don’t cut corners. Sinking crores on construction, non-compliance can lead to closure. Utilize the DPR phase by hiring an environmental consultant.

Find high-return business ideas based on your budget & ROI

Why Detailed Feasibility Reports Prevent Costly Mistakes

The main reason most CBG projects fail is due to poor feasibility studies. The entrepreneurs are misjudging the cost of feedstock, over estimating capacity utilization or under estimating working capital requirement. A well-executed techno-economic feasibility study “stress tests” the assumptions over a range of different scenarios, such as offtake contracts that are delayed, variations in feedstock costs, interest rate changes, lower than expected uptime etc.

Niir Project Consultancy Services prepares Market Survey cum Detailed Techno-Economic Feasibility Reports which are specialized reports for industry start-up projects. These reports outline manufacturing process flows, amount of units/demand in the market, list the suppliers for machines, outline raw material sourcing plan, and provide complete financials including profitability and break-even timelines. For entrepreneurs preparing CBG units, such reports help them determine if it is a commercial project prior to committing capital. That’s the difference between a planned entry and a shot in the dark.

A good DPR addresses difficult questions: What is the optimal feedstock mix in terms of procurement risk? What type of compression is most energy efficient? What impact does plant location have on the delivered cost to buyers? How much capacity will be required in order to service the debt? Are working capital requirements met by byproduct revenue? This is not an academic exercise; these are actual situations. They decide if your business is profitable or a “dead” asset.

Before approving term loans, Financial Institutions require feasibility reports. Demand estimates and competitive landscape are important to equity investors. A DPR will make you disciplined even if you are self-funding. It allows you to avoid over designing (wasting capex for unnecessary capacity) and under designing (not allowing economies to be realized because of premature limitation of scale). Take 3 months to do feasibility analysis. It saves the time of endless trial and error that would otherwise be needed.

Conclusion

In India, CBG production has progressed from experimental hobbies to a marketable manufacturing company, but it has not happened yet, and the process requires some learning and discipline to achieve a successful business. The sector has got great policy tailwinds, the technology is sound, offtake is guaranteed and clear profit paths. It is in line with national priorities: waste management, energy security, income generation in rural areas, and emission reduction.

Early-mover advantage is still in and it’s closing. Procurement costs will increase as more plants commission and more plants are looking to feedstocks. Those wishing to enter now can also get long-term supply contracts at good prices, develop deals with oil marketing companies and be allocated prime locations close to CGD networks.

Realism with regards to execution obstacles is a key to success. The process of aggregating feedstocks is not easy. Technological know-how is essential for plant uptime. If offtakes are delayed, a working capital cycle can put a strain on the finances. These are operation issues, not structural issues. In the past, Indian businessmen have shown their capability to carry out intricate manufacturing initiatives where the economic sense is there.

With the government’s announcement of mandatory blending of CBG starting FY 2025-26, it will become a growth market. Now that the demand for visibility has reached the Decade level. The investment is de-risked by RBI’s priority sector classification, capital assistance from MNRE, fertilizer subsidy on byproducts, and excise duty exemption.

Compressed biogas plants should definitely be considered in case of making a new manufacturing project. Do a proper feasibility study first. Identify feedstock sources. Seeing is believing: travel to working plants to learn about the reality. Discuss with oil marketing companies early on terms for procurement. Develop financial models with stress testing of assumptions. Collaborate with knowledgeable technology suppliers. Lock up land that is connected to gas supply.

The entrepreneurs who take action will undertake the feasibility analysis of their businesses with discipline and solve the logistical challenge of feedstock will be the entrepreneurs who will develop businesses which will respond to the Indian energy transition. The sector is real. The payoffs are attainable. The hazards are easily controlled. Now, execution capability and patient capital is required. The waste-to-energy (WtE) people who commit will find that it is not only good for the environment, it makes good business sense too.

Data Table: CBG Plant Investment & Returns by Feedstock Type

| Feedstock Type | Plant Capacity (TPD) | Capex Required (₹ Crore) | Gross Margin (%) | Break-Even Period (Years) |

| Agricultural Residue | 5 | 15-18 | 25-28 | 4-5 |

| Dairy Waste | 10 | 22-25 | 30-32 | 4-6 |

| Municipal Solid Waste | 20 | 35-40 | 18-22 | 5-6 |

| Agro-Processing Waste | 7 | 18-20 | 24-26 | 4-5 |

Frequently Asked Questions (FAQs)

Q1. How much is the initial investment required for setting up a CBG Plant in India?

The cost for setting up a viable commercial CBG plant is ₹15-18 crore for a 5 tonne per day unit based on agricultural residue. The capacity of 20 TPD is required in municipal waste plants, which cost between ₹35-40 crore. Additional working capital of 3-4 months’ operating expenses. The 70:30 debt-equity structuring is made possible by RBI’s priority sector lending.

Q2. What are the advantages to CBG entrepreneurs of the SATAT scheme?

SATAT has signed 20-year offtake contracts with oil marketing companies at indexed rates at ₹46-54/kg. It removes risk of demand. The scheme also provides linkage with various government incentives such as capital assistance from MNRE, waiver of excise duty on by-products, priority classification of loans by RBI, and subsidy on fertilizers.

Q3. What are the major operational challenges during the CBG manufacturing process?

Volatility in feedstocks is the highest risk. Capacity utilization is affected by seasonal availability, price variations and aggregation logistics. Poor gas yield is achieved due to mismatch between technology and feedstock type. Lack of grid connections raises transport costs. These risks can be well mitigated by appropriate feasibility studies and feedstock diversification.

Q4. What is the time to profitability of a CBG plant?

Typical break-even is in Year 4 to Year 6 based on feedstock costs, capacity utilisation and debt service. Plants that have a high uptime of 85-90% and multiple feedstock sources will achieve profitability sooner. The payback periods are drastically reduced if the organic manure and carbon credits are taken as byproduct.

Q5. What are the best areas for the establishment of CBG plant in India?

Agricultural residue plants are suitable for rice-wheat belt states (Punjab, Haryana, western UP). Dairy waste units in Gujarat, Maharashtra, Rajasthan. Municipal waste projects are preferred by Tier-2 cities suffering from landfill problems. Site selection should be done with the consideration of CGD networks and feed stocks within 100 km radius.

{kind=link}